The Stack Is Cracking: Why the World Is Switching Its Monetary Operating System

From Windows to iOS — how the dollar's architecture is losing coherence, and what the Asian alternative actually offers

The Invisible Architecture

Every analysis of the global economy begins at the wrong layer. Commentators debate whether earnings will beat expectations, whether the Fed will cut in September, whether China's property sector will drag on growth. These are legitimate questions. They are also, in structural terms, questions about the application layer — the visible surface of a much deeper architecture that most analysis never reaches.

The economy, properly understood, is not one system. It is three, stacked vertically, operating at different speeds, governed by different institutions, and failing through different mechanisms. The distinction between the economic system, the financial system, and the monetary system is not semantic. It is the difference between asking why an app crashes, why the middleware is congested, and why the operating system itself has stopped enforcing consistent rules.

Louis-Vincent Gave, building on decades of structural macro analysis at Gavekal, has articulated this tripartition with unusual clarity. His framework deserves serious attention not because it is politically convenient — it is not — but because it maps onto empirical realities that more conventional frameworks struggle to explain. Why did twenty years of quantitative easing not produce sustained growth? Why did the safest asset in the world, the US Treasury, become the epicenter of the 2022 bond crash? Why are central banks in the Global South buying gold at record pace while simultaneously taking on dollar-denominated debt? None of these phenomena make sense if you treat the monetary, financial, and economic systems as one continuous whole. They make immediate sense once you separate the layers.

This article attempts to do exactly that — and to follow the logic wherever it leads, including to conclusions that are uncomfortable for those who have internalized the post-1971 dollar order as a natural state of affairs rather than a contingent institutional arrangement.

Three Layers, One Stack

The cleanest way to understand the tripartition is through the analogy that Gave himself employs: the architecture of a computing system. The analogy is imperfect, as all analogies are. But it is precise enough to do real analytical work.

The economic system corresponds to the application layer. It is the world of firms, workers, supply chains, factories, ideas, and productivity. Amazon, TotalEnergies, Foxconn, a Vietnamese textile manufacturer, a French artisan — these are all applications. They solve concrete problems, produce concrete outputs, and generate real value. They are the visible surface of economic life. Crucially, applications can continue to function through changes in the layers beneath them. People still need to eat, travel, communicate, and manufacture goods regardless of what happens to the monetary architecture underneath.

The financial system corresponds to the middleware layer — the banks, capital markets, bond markets, private equity funds, insurance companies, clearing houses, and derivative structures that sit between the monetary base and the real economy. The financial system's function is to allocate resources: to take savings generated in one part of the system and direct them toward productive uses in another. It transforms maturities, pools risks, prices credit, and enables the coordination of capital across time and space. A deep, liquid, well-functioning financial system is like a high-performance middleware stack: it dramatically increases the efficiency with which the economy can execute its applications. A dysfunctional financial system — over-leveraged, misaligned, captured by rent-seeking — is like bloated, inefficient middleware that consumes resources without improving application performance.

The monetary system is the operating system. It defines the fundamental rules of the machine: the unit of account in which all prices, wages, contracts, and debts are expressed; the institutions authorized to create money; the rules of convertibility and exchange; and the governance framework that determines who can access the system and on what terms. The monetary system is to the economy what the OS is to a computer: you can run many different applications on it, but every application must ultimately operate within the rules it enforces. Changing the OS is the most disruptive thing you can do to the entire stack. It is also the rarest.

The critical insight that follows from this architecture is about the timescales and governance of each layer. Economic adjustments happen continuously — firms enter and exit, workers change jobs, supply chains reorganize. These are daily events. Financial adjustments happen in cycles — credit expansions, leverage buildups, crises, deleveraging — measured in years or decades. Monetary transitions are historical ruptures: the end of the gold standard in 1971, the creation of the euro in 1999, the Bretton Woods system from 1944 to 1971, the sterling system before that. They happen perhaps once or twice per century. When they happen, every layer above them is forced to reorganize.

We may be living through one now.

The Dollar as Windows

To understand the current transition, you need to understand what made the dollar-OS dominant in the first place — and what has changed.

The dollar did not become the world's reserve currency through superior monetary theory. It became dominant through a combination of geopolitical facts, network effects, and institutional depth that accumulated over decades. The Bretton Woods system established the dollar's primacy in 1944, when the United States held the majority of the world's monetary gold and produced approximately half of global industrial output. The Nixon shock of 1971 removed the gold anchor, but by then the network effects were so powerful that the dollar maintained its dominant position without convertibility. What replaced gold as the anchor was a combination of three things: the depth of US capital markets, the political and military power of the United States, and the liquidity of the Treasury market as a near-universal risk-free asset.

In the terminology of operating systems, the dollar is the Windows of global finance. Its dominance does not rest primarily on technical superiority. It rests on network effects, switching costs, and embedded dependencies. The vast majority of global trade is invoiced in dollars. The majority of sovereign debt, including debt issued by countries that trade primarily with each other and not with the United States, is denominated in dollars. The SWIFT messaging network routes dollar payments. The international financial system's plumbing — clearing houses, correspondent banking, margin requirements — was built around dollar liquidity. These are not incidental features. They are structural lock-ins that make switching from the dollar-OS prohibitively costly even when the system begins to exhibit serious bugs.

And the bugs have accumulated. The dollar-OS has been degrading for decades, though slowly enough that most users adapted rather than migrated. The Fed's repeated interventions — from the Greenspan put through the successive rounds of quantitative easing to the zero interest rate policy maintained for years after the 2008 crisis — gradually distorted the OS's core pricing mechanism. The Treasury market, which was supposed to be the system's risk-free anchor, became a heavily managed variable rather than a genuine market signal. The explosion of US fiscal deficits — from moderate to structural, from structural to seemingly permanent — undermined the long-term solvency logic that justified the Treasury's safe-haven status.

To return to the OS analogy: Windows has always had bugs. Users tolerated them because the switching cost was so high and the alternatives were not obviously better for their use cases. But there is a difference between ordinary bugs — slowdowns, occasional crashes, compatibility issues — and constitutional bugs: moments when the OS reveals that its security model has a fundamental flaw. The dollar-OS experienced its constitutional moment in 2022.

The Weaponization That Changed Everything

The freezing of approximately $300 billion in Russian central bank reserves held in Western financial institutions in February 2022 was the most consequential monetary event since Nixon closed the gold window. Its importance has been systematically underestimated in mainstream Western analysis, where it is treated as an exceptional wartime measure with limited precedent-setting value. This assessment is wrong, and its wrongness has real consequences for how we model the trajectory of the dollar system.

What happened in 2022 was not technically complex. Western governments — primarily the United States, the European Union, and the United Kingdom — invoked emergency powers to freeze assets held in their financial systems by a foreign central bank. The legal mechanisms were various: executive orders, EU Council regulations, UK statutory instruments. But the economic substance was uniform: money that a sovereign entity believed it owned, and had entrusted to another sovereign entity's financial system under the implicit promise of neutrality, was rendered inaccessible without prior judicial process or individualized finding of wrongdoing.

Charles Gave's characterization of this as a "1793 moment" — a reference to the revolutionary Terror — is analytically precise, not rhetorical. In 1793, the French revolutionary government demonstrated that property rights under the new regime were conditional on political alignment. The consequence was a massive flight of capital and human talent from France, a phenomenon that took decades to reverse. The 2022 freeze delivered an analogous message to every central bank outside the Western alliance: your dollar-denominated reserves are not property. They are an access privilege, revocable at the political discretion of the system's administrator.

The strategic implications cascaded immediately. For any country that does not have a security guarantee from the United States — and that is the majority of the world's countries by population, GDP, and resource endowment — the calculus for reserve management changed overnight. Holding Treasuries was no longer simply a question of yield and liquidity. It was a question of political risk. If the United States could freeze Russian reserves, it could — in principle — freeze Iranian reserves, Venezuelan reserves, Chinese reserves. The list of countries whose reserve managers drew this conclusion privately is long. The list of countries that began accelerating gold purchases, diversifying into non-Western financial instruments, or exploring alternative settlement mechanisms is documented and growing.

This is the mechanism by which the dollar-OS's structural degradation accelerated from a slow erosion to a visible fracture. The network effect that had sustained dollar dominance rested on a belief that the system was neutral — that using dollar-denominated assets was commercially rational regardless of your political alignment. That belief has now been falsified. Not for all users. Not even for most users yet. But for a significant subset of the system's large users, the risk model has changed permanently. And operating systems, like all network goods, can sustain considerable degradation without losing dominance — until they cross a threshold, at which point the network effects invert and reinforce the exodus rather than the inertia.

There is an additional dimension that Gave emphasizes and that deserves to be stated explicitly: extraterritoriality. The dollar system's architecture means that US law effectively governs any financial transaction that touches the dollar at any point. This gives US regulatory and intelligence agencies surveillance and enforcement authority over transactions between third countries that have no direct connection to the United States. For a European bank or an Asian commodity trader, operating in dollars means accepting permanent jurisdiction from a legal system they have no democratic relationship to. This is not a minor friction. For many actors, it has become intolerable.

The Asian Alternative Is Not a Mirror Image

It is tempting, having established the dollar system's fragility, to project a mirror image: a yuan-centered system that replicates the dollar's architecture with different branding. This projection is analytically wrong, and getting it wrong leads to systematic misunderstanding of both the opportunity and the risk in the emerging alternative.

The Gavekal framework, particularly as developed by both Louis-Vincent and Charles Gave, describes an Asian alternative that is architecturally distinct — not merely a competitor within the same paradigm, but a system organized around different principles.

The dollar system's anchor is political and military: the Treasury's safe-haven status rests ultimately on confidence in the permanence and reliability of US power. When that confidence weakens, the system has no other anchor. The emerging Asian system's anchor is, by contrast, commercial: the vast and persistent surplus of real goods that the Asian production complex generates relative to the rest of the world. China's trade surplus exceeded one trillion dollars in 2024. The broader Asian production zone's surplus with the rest of the world approached 1.4 trillion dollars. This is not a financial abstraction. It is a continuous generation of real claims on the world economy — goods delivered, services rendered, debts accumulated. A monetary system anchored in productive surplus has a fundamentally different risk profile from one anchored in political confidence. It can be wrong about many things and still maintain its core function.

The institutional architecture of the alternative system is equally distinct. Rather than a single reserve currency that all nations must hold, what is emerging is a network of bilateral swap lines in local currencies. The logic is straightforward: if China and Brazil have a swap arrangement, they can settle bilateral trade in their respective currencies without requiring either party to accumulate dollars as an intermediary. The network does not require a single dominant node. It is, in the terminology of network theory, more distributed — and therefore more resilient to the failure of any individual node, including the Chinese node itself.

The role of Hong Kong in this architecture deserves particular attention. China operates, in effect, a bi-monetary system: the renminbi for domestic transactions, with a controlled capital account that limits speculative flows and allows the state to direct credit toward industrial priorities; and the Hong Kong dollar — freely convertible, pegged to the US dollar — as the interface with international capital markets. This arrangement allows China to capture the benefits of international financial integration while insulating its domestic monetary system from the volatility that integration brings. It is, in the OS analogy, a virtualization layer: running the international financial environment in a sandboxed container that cannot crash the host system. Deposits in Hong Kong's banking system have grown dramatically — by some estimates exceeding $2.3 trillion, of which approximately $1 trillion is held in US dollars — representing a vast buffer that absorbs external liquidity shocks before they reach the mainland.

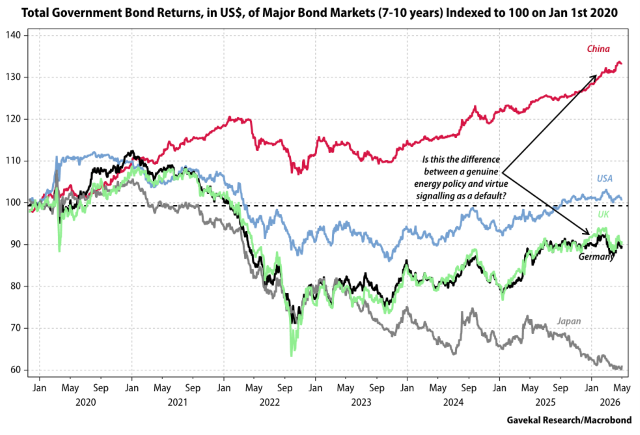

The bond market data provides perhaps the most compelling empirical argument. From 2004 to approximately 2020, Chinese ten-year government bonds, measured in total return terms and converted to US dollars, delivered the best risk-adjusted performance of any major bond market globally — outperforming Swiss bonds, US Treasuries, German Bunds, and dramatically outperforming Japanese bonds. This is a twenty-year record, not a single-year anomaly. It reflects the combination of positive real interest rates (a rarity in the Western world after 2008), controlled inflation, and managed currency appreciation. For an international investor constructing a store-of-value portfolio, the empirical case for Chinese bonds as an alternative anchor has been stronger than the theoretical arguments against it. Also, Chinese bonds have outperformed other major bond markets handsomely in 2026, the continuation of a well established trend (chart borrowed from Gavekal):

The Apple analogy, as applied to monetary systems, is clarifying here. Apple did not defeat Microsoft by building a better enterprise system. It built a system that was better for the consumer use case, capturing retail adoption before enterprise adoption, building network effects from the bottom up rather than the top down. The renminbi system is following an analogous path: it is not competing for dominance in the institutional finance market that the dollar controls — the market for sovereign debt, trade finance, and large corporate transactions denominated in dollars. It is competing in the markets the dollar system serves poorly: intra-Asian commerce, commodity settlement between the Global South, retail payments via digital platforms. It is winning in WeChat Pay and Alipay before it wins in SWIFT. The enterprise market — Western corporations, sovereign bond markets, global derivatives — may be the last to switch, just as enterprise IT was the last sector to migrate away from Windows.

But the architecture beneath that consumer adoption is not improvised. Two infrastructure projects — CIPS and mBridge — reveal the distinct logic of how the alternative plumbing is actually being laid, and it is worth treating them separately because they operate at different levels of the stack.

CIPS, the Cross-Border Interbank Payment System launched by China in 2015, is the RMB equivalent of CHIPS and Fedwire: a dedicated clearing and settlement rail for renminbi-denominated cross-border payments. It is not a messaging network like SWIFT; it actually moves money. By 2024, CIPS connected more than 1,600 direct and indirect participants across over 120 countries, processing tens of trillions of renminbi annually. In the framework of our three-layer stack, CIPS sits squarely in the middleware layer: it does not change the monetary OS (the renminbi remains a sovereign currency issued by the PBoC), but it provides an alternative financial plumbing that allows importers, exporters, BRI project finance, and commodity contracts to settle in RMB without routing through the dollar-correspondent banking system. Its strategic significance is precisely its interoperability: CIPS currently works alongside SWIFT rather than replacing it, but it provides a bypass route that can be activated progressively as the political cost of using dollar rails rises for more counterparties. It is the dedicated fiber backbone of the RMB-net, built parallel to the dollar-dominated internet of finance.

mBridge is a different beast, operating closer to the monetary layer itself. Developed jointly by the BIS Innovation Hub, the Hong Kong Monetary Authority, the PBoC, the Bank of Thailand, and the Central Bank of the UAE — with Saudi Arabia joining subsequently — mBridge is a distributed ledger platform on which multiple central banks can issue and exchange their own digital currencies (CBDCs) in real time, settling cross-border transactions in seconds rather than days, and executing FX conversion atomically between currencies without requiring a dollar intermediary. Where CIPS is an RMB rail within the existing monetary architecture, mBridge is a proto-hypervisor: a shared platform on which multiple monetary operating systems can run simultaneously, exchanging value directly through machine-executed contracts. If it reaches operational scale, it would not merely reduce dependence on the dollar correspondent banking system — it would make that system structurally irrelevant for any transaction between participating central banks. The pilot transactions conducted under mBridge have demonstrated the technical feasibility of this model. The political question — how many central banks join, and under what governance arrangements — remains open. But the engineering is done. The hypervisor exists. What remains is adoption.

What Comes After Windows

The history of technology transitions teaches a lesson that monetary analysts systematically ignore: incumbent operating systems do not fail because they become technically inferior across all dimensions. They fail because they stop serving the needs of a growing subset of their users, while simultaneously becoming less neutral — more politicized, more monopolistic, more extractive. The users who defect first are those for whom the cost of defection is lowest and the benefit is highest. Their defection reduces the network effects that sustain the incumbent, making it marginally more costly for the next tranche of users to stay, and so on. The transition is not a revolution. It is a cascade.

This is the mechanism at work in the current monetary transition. The countries driving de-dollarization are not doing so out of ideological commitment to multipolarity. They are doing so because the dollar-OS has become extractive — through financial sanctions, extraterritorial jurisdiction, inflationary dilution of reserves, and politically conditional property rights. Their defection is not yet catastrophic for the dollar system. But it is directional. And direction, compounded over time, is destiny.

What will replace the dollar-OS is not settled. The most analytically honest conclusion, consistent with both the Gavekal framework and the observable data, is that the transition leads toward a fragmented multipolar system rather than a clean hegemonic succession. The yuan will not become the next dollar in the sense of commanding equivalent global network effects. China does not want it to — running a reserve currency requires running structural trade deficits and opening the capital account, both of which would destroy the industrial surplus model that makes the Chinese system stable. What China wants, and what it is systematically building, is a network of bilateral arrangements that allow it and its partners to conduct commerce and settle debts without using the dollar as the intermediary. This is sufficient to achieve the strategic goal of sovereignty without requiring global monetary hegemony.

The practical investment and strategic implications follow from this architecture. Investors and policymakers who model the world as a binary choice between the current dollar system and a Chinese replacement are asking the wrong question. The right question is which assets and which institutional arrangements will retain their value across the transition — and which are specifically exposed to the failure modes of the incumbent system.

The failure modes of the incumbent system are now reasonably well identified. Long-duration Western sovereign debt is exposed to both fiscal deterioration and potential monetization. Dollar-denominated assets held in Western custodial systems are exposed to political confiscation risk for any entity that could plausibly fall outside the Western alliance. Financial institutions deeply embedded in the dollar middleware — correspondent banking, clearing houses, SWIFT-dependent payment chains — are exposed to structural bypass as alternative plumbing is built.

The hedges against these failure modes are also reasonably well identified: gold (the only reserve asset with no counterparty risk and no jurisdictional exposure), energy assets (which retain value in any monetary system because their utility is physical), and exposure to the productive surplus economies of Asia through their bond markets and equity markets. These are not contrarian bets. They are structural positions against identified risks in a system whose architecture is visibly degrading.

One final caution is warranted, and intellectual honesty demands it be stated clearly. The Chinese system, for all its structural advantages as described here, carries its own risks that are non-trivial. The opacity of Chinese financial statistics makes precise analysis difficult. The property sector remains a source of latent instability. The political concentration of authority in a single decision-maker introduces tail risk from policy error that is harder to hedge than the distributed dysfunction of democratic systems. And the historical record of monetary transitions suggests that even architecturally superior systems can fail during the transition itself — not because they are wrong in equilibrium, but because the path from here to there passes through episodes of extreme volatility that destroy capital and confidence regardless of the long-run destination.

The stack is cracking. The OS is being replaced. But transitions at this scale are measured in decades, not quarters — and the agents who navigate them best are those who can hold the long structural view without losing sight of the turbulence that surrounds it.